Add-on Insurance Scam Warning

IN THIS REPORT:

Many car buyers don't know they've been scammed

If you bought a car from 2013 to 2015 you are at risk - especially if you took the in-house finance

Check now if you are entitled to compensation

Full details: how to join the class action

CLASS ACTION:

Contact Bannister Law about the add-on insurance class action >>

If you bought a new car from 2013 to 2015 inclusive - and especially if you took the car dealer's in-house finance - you may have been sucked in by the add-on insurance scam.

The corporate watchdog, ASIC, calls it a "market that is failing consumers". If you are at risk, you might not even know you have purchased this kind of insurance. (Often, it was not properly disclosed.)

Download the full ASIC report >>

Read the ASIC media release >>

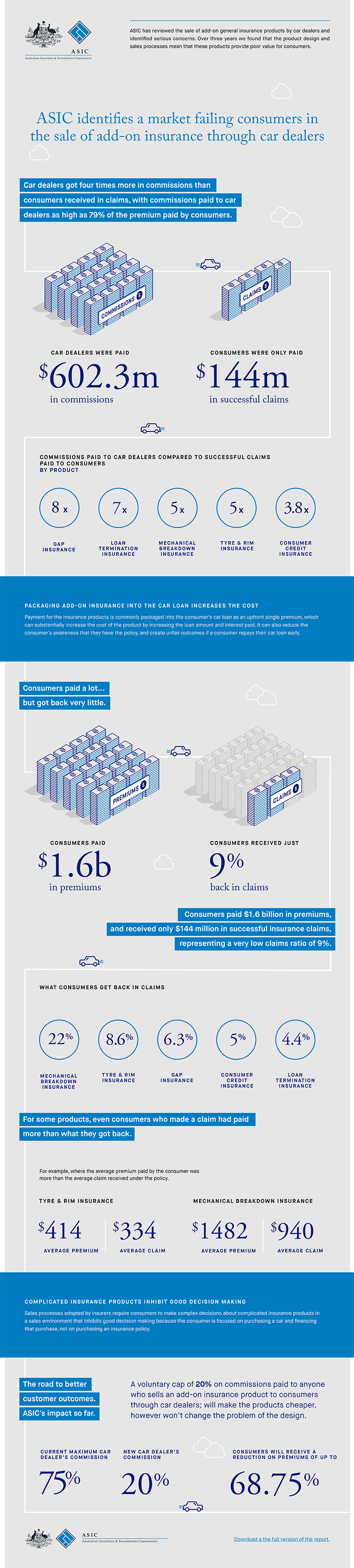

Scroll down for the video transcript. But first: here's the corporate watchdog's infographic snapshot on the add-on insurance scam

VIDEO TRANSCRIPT

Here’s what happens when car dealers and insurance companies get together, in private, and conspire to extract your cash…

It’s hard to imagine a more unholy alliance: car dealers colluding with insurance companies. It won’t end well for you, the consumer, if you start nodding along. In this report: an epic, orchestrated, corporate scam. An attack by stealth: selling you covert, complex insurance you don’t need, that isn’t explained, under the radar, where the price is extortionate and the cover on offer is at best minimal, and at worst, completely redundant and/or ineffective.

I’m John Cadogan, the founder of AutoExpert.com.au - the place where Australian new car buyers save thousands on their next new cars, without the entrenched rip-offs. To save, contact me here >> This report is about the grubby practice of covertly signing you up for so-called ‘add-on insurance’. If you, or anyone you know has purchased a car in the past three years, you might already be a victim of this scam, and you even might be entitled to compensation.

$1.6 BILLION RIP-OFF

The cashflow from this rort: huge - $1.6 billion raked in over three years, with a staggering $600 million of that simply pocketed by car dealers as outrageous, undisclosed commissions. Those commissions are more than four times what was paid out in claims. This is an epic ripoff.

When I found out about it, 10 days or so ago, I did what any self-respecting automotive shit-stirrer would do: I knocked on Channel Seven’s front door, and had a little chat to the news director.

People wonder why there’s widespread community opprobrium for both car dealers and insurance companies. Well, if there was any lingering doubt, out there, hopefully it’s sleeping soundly now. Certainly, when these two groups attack together … gestalt theory applies (the whole is greater than the sum of the component arseholes).

BANNISTER LAW INVESTIGATES CLASS ACTION

Charles Bannister is a consumer advocate, who’s taken on several corporate heavy hitters on behalf of ordinary Australians. He’s head-to-head with Ford over the notorious Powershift transmission. More on the Powershift class action >>

Right now, he’s investigating running a class action on the purveyors of this unscrupulous insurance.

"Class actions are representative proceedings in the Federal Court so you’d run the one lead plaintiff’s case and then you’d have the group or class of people behind them that have a same or similar loss and it allows to compensate the whole group of affected people.

"Seven or more people with a common claim can join together and commence a class action. It usually involves a lot more than seven people but the rules require seven people or more in order to commence representative proceeding.

"For a class action, if we decide to commence the class action, the lead plaintiff’s costs are the costs for running the whole action and then to quantify your individual costs will be a separate fee agreement to be retained as an individual client of the firm. So you can remain a part of the group, still be part of the action and not be our individual client, but as a group member, and not the lead plaintiff, you bear no risk in relation to a class action." - Charles Bannister

UNDER THE RADAR

So-called ‘add-on insurance’ is an attack by stealth, where the car dealer signing you up knows he’ll be pocketing as much as 79 per cent of any funds he can extract from you. And this attack takes place covertly, at the end of the endurance event you know and hate: buying a car. You know how this works - they wear you down at every turn. And they make it so easy to say ‘yes’.

You just go there for a car, right? And then, the long, distinguished list of extortionately profitable upselling begins. You meet the sales manager, whose job is really to gut you like the catch of the day. Some ageing fluffer named Tiffany tries to get you - excited - over the protection packages you don’t need, the over-priced accessories, the tinting, the saxophone holder, monogrammed luggage, the embossed genuine leopard print injection-moulded steering wheel bracket for your iPad - whatever.

And then they wheel out the F & I guy: the finance and insurance upsell is on. Somewhere along the line here - you might not even feel it - they slip in a little add-on insurance. Let’s call it what it really is: It’s bullshit insurance. And you know how I feel about all the different flavours of bullshit. My personal jihad...

WHAT IS ADD-ON INSURANCE?

You’re especially at risk of being scammed by this bullshit insurance if you took the in-house dealership finance (which I strongly advise you never to do). Bullshit insurance includes policies that allegedly cover your repayments in the event of sickness, injury, disability and death. It extends to cover you, allegedly, for the gap (if any) between what you owe on the finance and what you get if your car is written off in a crash.

There’s also loan termination bullshit insurance - which allegedly covers you for the gap between the value of the car and the amount you owe if you hand the car back because you get sick or injured and can no longer afford the payments. They’ll even offer to insure your wheels and tyres against damage, and then there’s the dreaded ‘extended warranty’ (which is really just a bullshit insurance policy dressed like a bad transvestite…)

That’s five different categories of bullshit insurance that generally doesn’t benefit anyone all that much, except of course the dealer selling it to you and the insurance company pulling the strings in the background.

"There was $1.6 billion collected over the three years from 2013 to 2015, and if you average it out between two and three thousand a policy then there’s between three hundred or five hundred thousand policies probably between the seven or eight insurers. It’s a lot of Australians, it’s a lot of new car purchases, it’s a lot of commissions going back to dealers. It’s $600 million that have been refunded to dealers as commissions.

"I’m not sure whether that was disclosed at the point of sale; for those people who knew about the purchase of the insurance product. It’s deeply concerning. The ASIC report is also very troubling." - Charles Bannister

THE CORPORATE WATCHDOG

The corporate watchdog, ASIC (the Australian Securities and Investments Commission) published a scathing report on insurance add-ons late last year. Sadly, I don’t know too many people who read ASIC reports recreationally, but if you ever thought, collectively, car dealers or insurance companies deserved the benefit of the doubt read that report. They are, most definitely, narcissistic, weapons-grade rip-off merchants. Or vampire sociopaths. Or both.

Not all insurance is bad. When you buy comprehensive car insurance, for example, most of the premiums are used to fund crash repairs and write-offs. Eighty-five per cent of those premiums is actually paid out in claims. And that seems fair. A 15 per cent margin. It’s reasonable. But with this bullshit insurance, only nine cents in every dollar is paid in claims. The mongrels selling it to you under the radar pocket more than four times the amount that will ever be paid in claims, as commission. And the arsehole insurers keep the rest. Good for them, bad for you.

And by ‘arsehole insurer’ I mean seven of the nation’s largest insurance giants. Just detain yourself for a moment while you consider the breathtaking bipolarity of these corporate cocks. Consider the squeaky clean, even friendly, advertising…

...and then, in contrast, their sociopathic willingness to bend you over, with undignified intimacy, using carefully engineered bullshit insurance add-ons.

"I think that creates an environment of car salesmen being incentivised to that extent of them saying really anything and everything in some circumstances to get the sale of the insurance product over the line so they can reap their commission. That’s dangerous territory in putting those level of incentives in car dealers’ hands.

"I would go and check your purchase invoice. If you don’t have a copy of it, the finance company that you leased the vehicle through definitely will. That invoice should have on it, especially if the insurance was financed at component or line item in the invoice for the insurance part.

"Once you’ve seen that you’ve got insurance, whether you knew about it or in most cases, you won’t know about it, then you should join the class action and register online.

"At the moment, it’s under investigation. However, we are having hundreds of people contact us with a common thread. I would say at least fifty per cent of the registrations so far have revealed that people didn’t know that they had the insurance when they purchased the car. So they’re finding out after they’ve purchased the car that the insurance was also included.

"There’s a large percentage of people also that were told they wouldn’t have the finance approved unless they took out the insurance. So that’s misleading." - Charles Bannister

WILD, WILD WEST

Selling this insurance was the wild, wild west of the commercial car-dealing landscape about three years ago. It’s hard to imagine a more profitable part of the deal. Dealers even set their own pricing for these products - whatever they could get away with. And that means some consumers paid 10 times more than others for exactly the same product.

ASIC even found that one of these insurance arseholes went so far as to train car dealers in how to avoid disclosing the actual cost of the premium, even if asked directly, during the sales process. They certainly provided scripts, so everyone could sell from the same grubby hymn book, published in consumer hell.

ASIC also found some bullshit insurance policies were completely unnecessary - such as extended warranties. These do not actually give you any more protection than the consumer guarantees under existing Australian Consumer Law. They also found numerous instances of overlapping cover - where multiple add-ons, all sold to you individually - essentially cover you for the same thing.

COMPLEXITY IS KING

And, of course, they found bullshit insurance policies were wilfully designed to be too complex to understand - especially in the context of a snap decision presented to you on the showroom floor, when you’re really just there to buy a car.

ASIC found a bullshit smorgasboard of up to 10 add-on insurance products from one insurer, all with multiple options. The maximum from one arsehole insurance giant was a brain-bending 224 different permutations of options and cover levels. This is at the end of the already arduous endurance event we know and hate: the car-buying process itself.

So, in short: this ASIC report and the $1.6 billion bullshit insurance scam is another great reason never to buy anything other than just the new car from any car dealer. Do not open the door to these kinds of covert attacks - because they’re very sophisticated, and they’re designed for one thing: to get you looking the other way while the Dyson goes deep in your wallet.

These bullshit insurance products are things you do not need. They’re extremely poor value, and another example of what happens when regulatory oversight is inadequate, and car dealers are struggling to pump up their profitability in the face of falling retail margins. The commercial model for selling new cars is bending, and one day soon, it will foreseeably break.

SCAM Vs TRUST

The ASIC report, and Bannister Law’s consumer advocacy, is one more stress fracture on that commercial rip-off merchant pillar. Car dealerships are gagging for disruption - they’re crying out to be Uber-fied. But until that happens, you need to protect yourself by just saying ‘no’ at every turn. Because they are completely unafraid to greet you and gut you at any opportunity. And I’m tipping you aspire to be more than simply some car dealer’s sashimi.

If you - or someone you know - purchased a new car any time in the past three years, now is an excellent time to review all the paperwork and reach out to Charles Bannister, because you just might have a claim.

If I were a carmaker I would be extremely concerned about the conduct of my dealers. And altruism would not fuel that concern. Buying any car - choosing that brand - is about trust. This is a primary ‘buy in’ criteria. And I cannot for the life of me imagine commercial conduct on any retail landscape that is better designed to break that bond of trust with a brand.

Customers don’t see the distinction between the brand and the dealer. So if the dealer is an unscrupulous arsehole, therefore, so is the brand. That’s how this plays. The two have been carefully designed to seem one and the same. It’s the brand up there in lights, after all. And it seems to me that selling bullshit insurance is a great way to tarnish the brand. Of course, on planet ethics, it’s also clearly the wrong thing to do. If that matters.

You might of course also like to reach out to your insurer, too, and tell them exactly what you think - especially if you are also insuring your house, the car or the business with them. And you can reach out to me via the website if you need a new car and you just dread going head-to-head with one of those mongrels. Make sure you check that paperwork. I’m John Cadogan. Thanks for watching.